Specific funds can have their own timelines, financial investment objectives, and management philosophies that separate them from other funds held within the same, overarching management firm. Successful private equity companies will raise many funds over their lifetime, and as companies grow in size and intricacy, their funds can grow in frequency, scale and even specificity. For more information about private equity and also - visit the videos and -.

Prior to founding Freedom Factory, Tyler Tysdal handled a development equity fund in association with a number of celebs in sports and home entertainment. Portfolio business Leesa.com grew quickly to over $100 million in incomes and has a visionary social mission to “end bedlessness” by donating one mattress for each ten sold, with over 35,000 contributions now made. Some other portfolio companies remained in the industries of wine importing, specialty loaning and software-as-services digital signs. In parallel to handling properties for companies, Ty was handling private equity in real estate. He has had a number of successful personal equity investments and a number of exits in student housing, multi-unit real estate, and hotels in Manhattan and Seattle.

Managing Director/ Partner – In charge of leading the firm’s investment focus and technique, along with handling relationships with investors and raising new funds. $ million cobalt. – Take part in financial investment decisions, sit in the financial investment committee, and sit on the portfolio companies’ board. – Compensation is largely driven by profits of the firms.

An intro to private equity in 5 sections: (1) Definition and structure of the industry (2) Buyout funds (3) Venture funds (4) Development/Growth funds (5) Due Diligence and other topics – $ million investors. The asset about this book is that it doesn’t get overly technical from the start, however takes some time explaining the organisation design of private equity companies in basic.

This book is mostly about the development of scrap bonds, which are the kind of financial obligation utilized to fund Leveraged Buyouts (LBOs), without which the private equity market would not truly exist. The books concentrates on the rise and fall of famous investment bank Drexel Burnham Lambert, the bank that ruled the junk-bond world in the ’80s.

This book relates the real story of a bidding war for RJR Nabisco (one of the biggest consumer items company in the U.S. at the time), who was eventually obtained by KKR. We recommend this book due to the fact that it is well-written and relates to a true, extremely crucial occasion of financial history; also, it will give you a good idea of the political fights that take place throughout large leverage buyouts.

This is a research study of private equity leader and powerhouse KKR. This is an excellent read for numerous reasons; it not only provides you an unbiased story of KKR’s rise to prominence, but it also information other elements of private equity such as deal structuring, definitions of technical terms, and an intriguing insight into entrepreneurship.

How To Answer “Why Private Equity” For Interviews – 10x Ebitda

.png?width=600&name=How-to-Choose-the-Best-Private-Equity-Firm-Chart%20(2).png)

China is not only a book about doing service in China. It tells the real story of a hard Wall Street banker pertaining to China to purchase business, ultimately spending $400m buying Chinese business in the ’90s, with somewhat disastrous (and in some cases humorous) results. It is incredibly well-written, and supplies an excellent insight into doing private equity in China, and likewise about how challenging it is for private equity firms to manage and turn around the business they buy – civil penalty $.

The list listed below is a high-level explanation of the various types of debt instruments that are typically used in LBO deals. When purchasing a business, the private equity fund will normally provide anything between 30% to 50% of the purchase rate in equity (i. tyler tysdal business.e. the fund’s own money), and obtain the rest.

The type of financial obligation used, in order of threat (from the financing bank’s perspective), consists of: This debt ranks above all other debt and equity capital in the organisation, suggesting it needs to be paid back before other loan providers can get any cash. The financial obligation has very stringent requirements (i (conspiracy commit securities).e. must abide by particular monetary ratios), and is generally secured versus particular possessions of the business.

For that reason, it has the most affordable rate of interest of all these types of financial obligation and, from the lender’s point of view, this is the most protected form of financing. Financial obligation payments can be spread out over a 4 to nine-year duration or be paid in one last payment in the last year. This financial obligation ranks behind senior financial obligation in order of priority on any liquidation.

The requirements of the subordinated debt are usually less stringent than senior financial obligation, but because subordinated debt gives the loan provider less security than senior financial obligation, lending expenses are usually higher. This is usually high-risk subordinated financial obligation, and ranks behind senior financial obligation and unsecured debt. Interest on mezzanine debt is much greater, however while part of the interest requires to be paid in money, another part (called a PIK, or “paid in kind”) is rolled up into the principal.

What Is Private Equity – Pomona Investment Fund

/dotdash_Final_Private_Equity_Apr_2020-01-3ce99c81ce344ddc94fe05b17a2b7716.jpg)

Therefore, the following year, you will need to pay 10% on the brand-new principal of 100 + 5 accrued in previous year (which equates to 105), and this continues up until maturity when the full principal needs to be repaid (usually within 10 years). In some cases the mezzanine financial obligation will also consist of warrants or alternatives so that the loan provider can participate in equity returns.

But what do private equity experts truly do on an everyday basis? The time of private equity professionals is divided between four primary categories: This task is mainly carried out by the senior partners in a private equity fund, however in some cases a devoted fundraising group will work within some of the larger funds.

This goes in cycle: when the existing fund is close to being fully spent (i.e. 70-80% of the cash has been invested in companies), the senior management will go on the road and request fresh money – securities exchange commissio. Fundraising includes presenting the past efficiency of the fund, its strategy, and the people working in the firm who will supervise of making financial investments.

The “sourcing” (i.e. discovering financial investments) part is mostly done by mid-to senior management, and involves searching for possible targets and reaching out to the management of those business, either directly or through an intermediary such as an investment bank. Lots of private equity funds will specialise in sectors and/or areas; their devoted teams will have really strong knowledge of all the appealing business in a particular sector and will also know potential targets’ management groups well.

This includes drilling into the monetary efficiency of the company, analysing the trends in the industry, working out with the target, and collaborating the work of consultants: financial investment banks, accounting professionals, technique consultants, attorneys, technical experts, and so on. Once they have analysed sufficient information, the group will provide an “investment paper” to the senior partners to propose the investment.

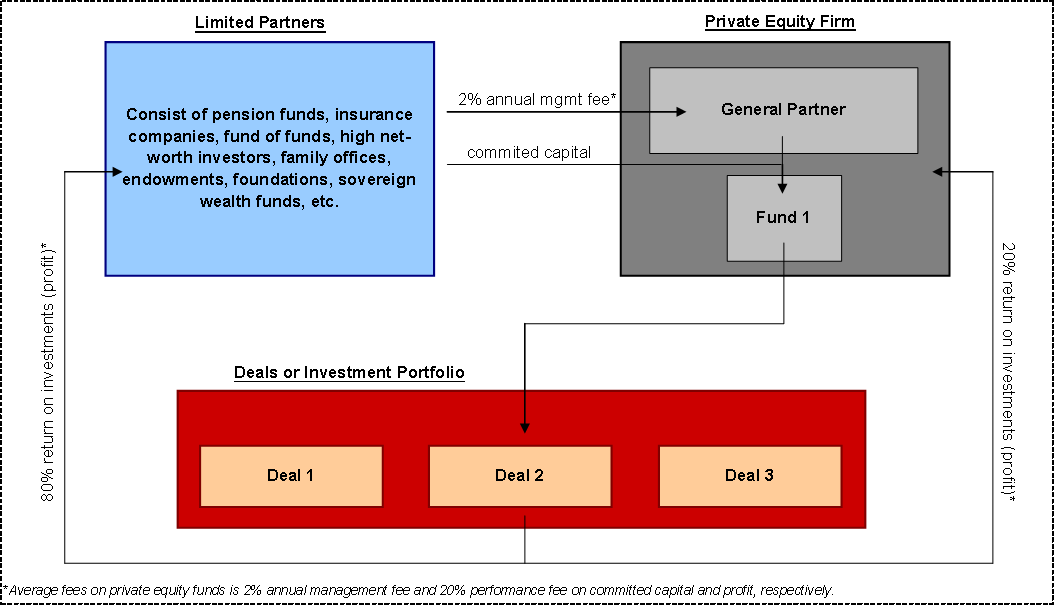

How Private Equity Firms Are Structured?

Once a business has actually been obtained, it requires to be managed for a couple of years until it is sold off. While private equity experts are not involved in the everyday running of the companies they buy, they will monitor performance and be involved in crucial strategic choices. While some firms have expert teams that handle financial investments (” operations teams”), many of the time the group that worked on the transaction will be in charge of keeping an eye on the company.

Investments are typically kept for 3 to five years, and will be offered after that time duration. This procedure is also normally handled by the more junior team under senior management supervision. Business can be sold though a sale to another company, a sale to another private equity firm, or by means of an IPO on the stock exchange.

Nevertheless, those who handle to make the switch to Private Equity usually do so at an extremely young age, either in their mid-twenties or early thirties. So, do they keep operating in private equity for the next 30 years? Can they alter jobs? Below is an overview of the potential profession exits available to private equity specialists.

If you work in private equity, you will not be able to end up being millionaire overnight – it will take a minimum of 5 to 10 years. Therefore, a lot of PE professionals decide to relocate to hedge funds, where returns can be made quickly and cash can be made (but also lost) more quickly.